As readers of The Target Report know, we view the printing, packaging, and related industries from the perspective of M&A transactional activity. Over the past eleven years, we have chronicled, logged, and commented on the robust merger and acquisition activity in the print-centric business segments. We traditionally take a break at this time of the year, depart from our usual review of the prior month's deal activity, and take a look back at the past twelve months from a high-level macro perspective. Our goal in this annual review process is to identify some long-term trends. Which segments have experienced more, or less, deal activity? What are the trends in the buyers’ rationale to complete these acquisitions? Are acquirers adding facilities to their networks, or opportunistically folding acquisitions into their existing facilities?

We review, categorize, sort, count, and chart the data we have collected, comparing the trailing twelve months (“TTM”) ended this August to the prior twelve months. This year we include the prior three years which bridge the pandemic period. This provides an illustration of the business climate in the printing, packaging and related industries: pre-pandemic, pandemic, and the current post-pandemic sweet spot.

In pure numeric M&A terms, the past twelve months were on par with the twelve months ended August 2021 and the twelve months ended August 2019. We identified approximately 217 transactions of interest during the past twelve months; compared to 218 last year. And 215 in the TTM August 2019. In the period ended August 2020, without question the period in which most companies took the biggest hit from Covid, we identified only 192 transactions in the segments we track, or otherwise stated, an 11.5% reduction from the norm of the three surrounding years. The market has moved on and Covid is in the rearview mirror.

As illustrated in the chart below, deal activity spiked upwards in the autumn of 2018 and again at the beginning of 2020. For reasons that were never clear, at least not to us, there was a pronounced slump in deal activity during the beginning months of 2019. Activity returned to the norm in the Spring of that year. Most dramatic and no surprise to anyone, there was a steep decline in transactions during March and April of 2020 when Covid-19 broke out and much business and social activity came to a screeching halt. Beginning not long after, in August of 2020, deal activity had returned close to the norm and has continued apace ever since, with another cooling-off period last winter and early spring during the spread of the Omicron variant. The trend is now headed upward as indicated by the purple line representing the latest trailing twelve-month period.

Looking at the gross numbers of M&A deals provides a view of overall transactional activity. However, as we know, the printing industry is not monolithic. Rather, in addition to the more generalized commercial printing business, the placement of images via ink onto a variety of substrates is comprised of a complex mix of specialties, including direct mail, wide format, industrial printing, and several forms of packaging. In our search to understand the market better, we categorize all the deals we have logged over the past eleven years by segment. We then dig deeper into the packaging, commercial printing, direct mail and wide-format printing businesses, illustrating the rationale behind all this deal activity, by segment. We also seek to understand where the business challenges facing owners are most pronounced by studying bankruptcy filings and non-bankruptcy plant closings.

The next chart breaks down the M&A transactions over the past four years into all the segments we track in The Target Report.

Commercial Printing

Our annual deep dive into the rationale behind the transactions in the commercial printing segment reveals a meaningful change in the market. There are significantly fewer transactions structured as tuck‑ins within the commercial segment, both in absolute numbers and as a percentage of the total. In fact, the decline in the number of transactions in the commercial printing industry is almost entirely attributable to fewer companies closing up and moving their business over to the buyer’s production facility.

In these tuck-in transactions, the customers of the acquired company are transitioned to the buyer’s production facility. Buyers will often leave the disposition of the plant and equipment to the seller, or to the seller’s agent, avoiding responsibility for trade and other debt, and possibly cherry-picking certain equipment that is needed or desirable for the smooth continued servicing of the acquired customers.

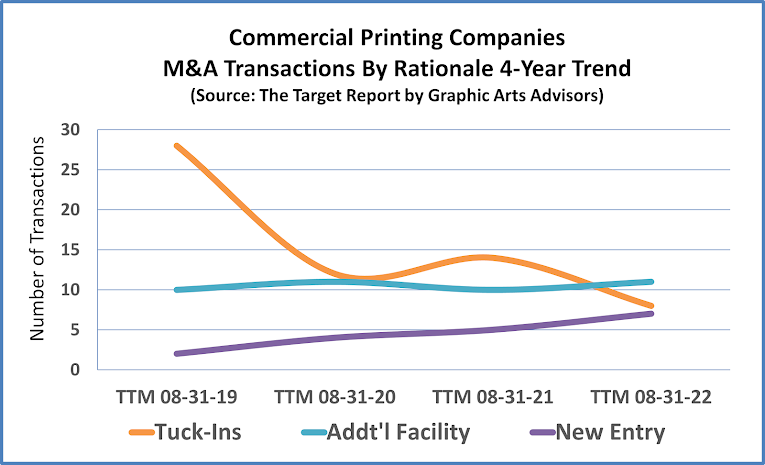

Back in August of 2019, when we first began digging deeper into the rationale behind the industry M&A transactions, the percentage of deals in the commercial printing segment structured as a tuck‑in was a staggering 70%, a clear indication of overcapacity and likely a necessary shuttering of shops burdened with out-of-date technology. The percentage fell dramatically during the following two years to 44.4% and 48.3%, respectively. In the twelve months just ended, tuck-ins represented only 30.8% of the total. In absolute numbers, there were only eight tuck-ins in the most recent year, compared to twenty-eight noted in the 2019 analysis. This decline in tuck-in transactional activity indicates to us that there is less excess capacity in the current market.

There were 18 acquisitions in the commercial printing segment where the acquired facility was important to the buyer and will remain in operation, as-is-where-is. Seven of these were sold to “new entry” owners that were not previously invested in the commercial printing industry. Notably, the number of transactions in commercial printing that were completed by these new entrants increased in each of the past four years, from only two in 2019, then four, then five, and now seven in the latest year. Outsiders are once again interested in investing in the printing industry.

The following chart shows how the past four years compare, showing tuck-ins, existing businesses adding facilities, and new entry owners into the commercial printing business.

Digging a little deeper, we looked for instances in which buyers cited geographic expansion and/or added services as the rationale behind their acquisitions, as well as whether a private equity sponsor was involved. Expanding service territory is still the reason most often mentioned, but now followed closely by the desire to add a new service, a return to the earlier trend. Notably, many of the transactions were part of a clearly expressed strategy to grow regionally in a hub-and-spoke fashion with a core financially strong commercial printing company at the center (see The Target Report: Commercial Print Awakes from M&A Slumber – June 2022). This regional consolidation trend has been in contrast to a couple companies executing a national roll-up strategy (e.g., JAL Equity and BR Printers) and clearly different from the disintegrated roll-ups from years past (see The Target Report: Cenveo Returns to its Roots – July 2022).

Many owners we talk with in the commercial segment tell us that their shops are quite busy. They share with us that their company is returning to and exceeding their pre-pandemic revenue. Availability of trained labor and limited paper supply have become the constraints on the business, rather than lack of customer orders. Almost without exception, owners we talk with are raising prices and they tell us that their customers are accepting the increases with less objection than experienced in many years. (We hear these comments across the various printing and packaging segments, not just from commercial printers).

Owners that had put their exit plans on hold are now ready to get back into the market or are already actively seeking a buyer. We expect that trend to continue and increase over the next couple of years. Consolidation will pick up steam as the impact of government subsidies fades, while balance sheets are still flush with cash, and hopefully before the next adverse event (storm, virus, attack, recession, etc.) The demographic imperative of an aging population is a strong driver for owners in the commercial segment to bring their companies to market. It is time to cash out rather than sign up for another round of investment and related long-term debt.

In another change in the market, private equity has warmed up to the commercial printing segment. We noted seven commercial print transactions in which private equity supported the transaction during the past year, a meaningful increase from the prior years.

Packaging

The packaging business is now the most active among the segments we track, by a factor of three-to-one over the number two segment, commercial printing. Packaging deal activity was red hot last year and heated up even more over the past twelve months. A multitude of private equity investment funds are driving transaction multiples up and up as they compete to consolidate a highly fragmented industry. Many packaging companies are family-owned, spanning two or more generations. At Graphic Arts Advisors, we have heard several credible stories of offers from private equity funds that out-of-the-gate open the conversation with suggested offers in the double-digits, irresistible opportunities to monetize and diversify family wealth.

The following chart is illustrative of buyer activity in the packaging business, broken down by primary product produced at the target company. Label manufacturing retains the lead in terms of number of transactions. The corrugated box segment has remained relatively quiet; once again we suspect because the low-hanging fruit has already been picked, not because there are any fewer boxes showing up on our front porches. The flexible packaging segment continues to be of keen interest to buyers, however the number of deals is constrained in some degree by the limited number of targets compared to other packaging segments. Also worth noting is the steady uptick in transactions in which folding cartons are the primary product of the target company. We expect that trend to continue as private equity funds seek alternatives to the higher multiples in the label and flexible packaging businesses, as well as in response to social trends extolling the use of more sustainable fiber-based packaging (see The Target Report: Label Roll-Ups are Red Hot; Are Folding Cartons Next? – March 2022).

Our candidate for the most interesting development in the packaging segment during the past twelve months is the emergence of GPA Global as a roll-up bringing together traditional asset‑light outsourcing expertise with domestic production capabilities, both in the US and Europe. The moves by GPA to add localized production are indicative of the larger economic trend of onshoring brought on by the Covid pandemic and international political tensions. (See The Target Report: GPA Global Emerges as Packaging Consolidator – December 2021). GPA’s resulting network of packaging and printing plants bridges the US with west and east coast locations. The acquired former ASG Print operations in Poland serve the European market for GPA Global. (We have noted that the industrial printing segment in the US has also been positively impacted by this onshoring trend.)

When we dig into the rationale behind transactions in the packaging segment, a very different picture emerges as compared to commercial printing. Of the 74 transactions that we recorded over the past twelve months in the packaging segment, only three were reported to be tuck-ins; two were relatively small and produced labels, the third was the divestiture of a specialty flexible packaging division in a sale in pieces of a company that primarily produced packaging films. In most of the other cases, the buyers noted that the acquired location was an important element of the rationale to complete the deal. In some, the acquired company had multiple locations, or was global in scope. An increasing number of the packaging companies, fifteen over the past year, were sold to new owners that were not currently invested in this segment, a continuation of the trend over the past four years.

Back in August of 2019, when we first began digging deeper into the rationale behind the industry M&A transactions, the percentage of deals in the commercial printing segment structured as a tuck‑in was a staggering 70%, a clear indication of overcapacity and likely a necessary shuttering of shops burdened with out-of-date technology. The percentage fell dramatically during the following two years to 44.4% and 48.3%, respectively. In the twelve months just ended, tuck-ins represented only 30.8% of the total. In absolute numbers, there were only eight tuck-ins in the most recent year, compared to twenty-eight noted in the 2019 analysis. This decline in tuck-in transactional activity indicates to us that there is less excess capacity in the current market.

There were 18 acquisitions in the commercial printing segment where the acquired facility was important to the buyer and will remain in operation, as-is-where-is. Seven of these were sold to “new entry” owners that were not previously invested in the commercial printing industry. Notably, the number of transactions in commercial printing that were completed by these new entrants increased in each of the past four years, from only two in 2019, then four, then five, and now seven in the latest year. Outsiders are once again interested in investing in the printing industry.

The following chart shows how the past four years compare, showing tuck-ins, existing businesses adding facilities, and new entry owners into the commercial printing business.

Many owners we talk with in the commercial segment tell us that their shops are quite busy. They share with us that their company is returning to and exceeding their pre-pandemic revenue. Availability of trained labor and limited paper supply have become the constraints on the business, rather than lack of customer orders. Almost without exception, owners we talk with are raising prices and they tell us that their customers are accepting the increases with less objection than experienced in many years. (We hear these comments across the various printing and packaging segments, not just from commercial printers).

Owners that had put their exit plans on hold are now ready to get back into the market or are already actively seeking a buyer. We expect that trend to continue and increase over the next couple of years. Consolidation will pick up steam as the impact of government subsidies fades, while balance sheets are still flush with cash, and hopefully before the next adverse event (storm, virus, attack, recession, etc.) The demographic imperative of an aging population is a strong driver for owners in the commercial segment to bring their companies to market. It is time to cash out rather than sign up for another round of investment and related long-term debt.

In another change in the market, private equity has warmed up to the commercial printing segment. We noted seven commercial print transactions in which private equity supported the transaction during the past year, a meaningful increase from the prior years.

Packaging

The packaging business is now the most active among the segments we track, by a factor of three-to-one over the number two segment, commercial printing. Packaging deal activity was red hot last year and heated up even more over the past twelve months. A multitude of private equity investment funds are driving transaction multiples up and up as they compete to consolidate a highly fragmented industry. Many packaging companies are family-owned, spanning two or more generations. At Graphic Arts Advisors, we have heard several credible stories of offers from private equity funds that out-of-the-gate open the conversation with suggested offers in the double-digits, irresistible opportunities to monetize and diversify family wealth.

The following chart is illustrative of buyer activity in the packaging business, broken down by primary product produced at the target company. Label manufacturing retains the lead in terms of number of transactions. The corrugated box segment has remained relatively quiet; once again we suspect because the low-hanging fruit has already been picked, not because there are any fewer boxes showing up on our front porches. The flexible packaging segment continues to be of keen interest to buyers, however the number of deals is constrained in some degree by the limited number of targets compared to other packaging segments. Also worth noting is the steady uptick in transactions in which folding cartons are the primary product of the target company. We expect that trend to continue as private equity funds seek alternatives to the higher multiples in the label and flexible packaging businesses, as well as in response to social trends extolling the use of more sustainable fiber-based packaging (see The Target Report: Label Roll-Ups are Red Hot; Are Folding Cartons Next? – March 2022).

Our candidate for the most interesting development in the packaging segment during the past twelve months is the emergence of GPA Global as a roll-up bringing together traditional asset‑light outsourcing expertise with domestic production capabilities, both in the US and Europe. The moves by GPA to add localized production are indicative of the larger economic trend of onshoring brought on by the Covid pandemic and international political tensions. (See The Target Report: GPA Global Emerges as Packaging Consolidator – December 2021). GPA’s resulting network of packaging and printing plants bridges the US with west and east coast locations. The acquired former ASG Print operations in Poland serve the European market for GPA Global. (We have noted that the industrial printing segment in the US has also been positively impacted by this onshoring trend.)

When we dig into the rationale behind transactions in the packaging segment, a very different picture emerges as compared to commercial printing. Of the 74 transactions that we recorded over the past twelve months in the packaging segment, only three were reported to be tuck-ins; two were relatively small and produced labels, the third was the divestiture of a specialty flexible packaging division in a sale in pieces of a company that primarily produced packaging films. In most of the other cases, the buyers noted that the acquired location was an important element of the rationale to complete the deal. In some, the acquired company had multiple locations, or was global in scope. An increasing number of the packaging companies, fifteen over the past year, were sold to new owners that were not currently invested in this segment, a continuation of the trend over the past four years.

Private equity was involved in 56 of the 74 total transactions in packaging, 69% of the total, comparable to the past year on a percentage basis, an increase of twelve transactions in absolute terms. The roll-up model, with financial sponsorship from private equity, is still in full swing across the various packaging segments and as we have noted repeatedly over the past two years, is driving competition for midsize and larger label printing companies to a frenzied level of activity. Adding to the hustle, fifteen new players entered the packaging business last year, and nine of these were backed by private equity firms establishing a new platform for further acquisitions.

Seven of the buyers noted that the acquisition brought new services to the company, or significantly expanded on a small beachhead previously established in that service. For example, in January, Avery, a division of Canada-based CCL Industries, acquired International Master Products, a US manufacturer of horticultural labels and tags. They bolstered the new specialty four months later with another acquisition, the purchase in the Netherlands of the Floramedia Group, another specialized producer of horticultural labels and tags.

In seventeen instances, geographic expansion or diversity of the acquired locations was noted as a key element in the buyer’s logic. While fewer in number than reported last year, an expanded geographic footprint still looms large in buyers’ expressed logic for completing acquisitions.

For our purposes in forming a picture of the various market segments that comprise the overall print-centric industries, we separate out companies that produce mostly wide-format and related products from the more generalized commercial printing segment. We include retail display and trade show graphic production in this category, as well as the expanding business of indoor architectural environment graphics.

In a complete inverse of the Covid impact on the packaging segment, which thrived during the pandemic, the wide-format market took a big hit. Event, trade show, and retail graphics all came to a screeching halt in the Spring of 2020 and are only now approaching pre-pandemic volumes according to many owners we speak with. The trends we noted in the past are still evident; gone are the days of the uniqueness of digitally printed banners and wraps, the cool factor of flatbeds has chilled, and the easy margins that came with being first on the block to offer large inkjet prints have been compressed by competition. Pricing on entry-level equipment has come way down, finishing technology is automated, and overall barriers to entry are low. Differentiation in the wide-format business has moved from first-mover advantage to more complex online direct-to-customer systems, robust planning and installation capabilities, or value-added services such as framing prints for use as home or office décor.

Despite the challenges of the past two years, interest in the wide-format segment appears ready to resume as life returns to a post-Covid normal state. A notable example over the past year was the acquisition of Screaming Images, a wide-format printing company in Las Vegas, well-positioned to benefit from the resumption of events in America’s adult playground that doubles as a mecca for trade shows. Geographic diversity was cited by the buyer, Milwaukee-based Olympus Group, as the driving criteria for the purchase. The acquisition brings the company’s footprint to five locations, ranging from Nevada to Florida.

In the wide-format and related products segment, there are proportionately fewer tuck-ins than in general commercial printing. Consistent with the decline in transactional activity over the past two years, there were only two wide-format tuck-ins during the past year, with the seller’s plant shuttered and production consolidated in the buyer’s existing facility. While tuck-ins are usually indicative of excess capacity and with the maturation of the wide-format segment, we frankly expected more transactions as this segment was hit hard. Many wide-format shops pivoted to producing personal protection equipment and warning signage, something that they were especially well-suited for with flatbed cutters and the capability to print floor graphics. Nonetheless, we expect that there are some weaker players in the market and tuck-ins will pick up in this segment.

Three buyers noted geographic expansion as important to their decision to move forward during the past year, consistent with prior years and with the stresses on wide-format in the pandemic period. Three buyers cited adding or greatly expanding wide format as a service offering as the logic supporting their acquisition.

Only one transaction in the wide-format segment was backed by private equity, the purchase in August of AllOver Media by ShoreView Industries. AllOver Media, based in Minneapolis, specializes in out-of-home advertising including billboards and transportation graphics. The transaction represents a new platform company for ShoreView.

Despite the lull in wide-format transactions, the existing presence of several private equity-backed platforms in the segment portends more activity to come. We continue to believe that the trends in wide-format and related printing, especially the involvement of financial buyers and the smattering of distressed transactions, as noted below, are predictive of increased future M&A activity and consolidation for wide-format printing companies.

Direct Mail

Direct mail printing companies, especially those that can manage, manipulate, store, and utilize data to drive improved results for their customers, are an exception and in a class by themselves, apart from the more generalized undifferentiated “job-shop” commercial printing companies that happen to include some mailing capabilities. Therefore, we break out these highly specialized direct mail companies into a separate segment for analysis.

Transactional activity in the direct mail printing segment declined over the past twelve months, with a total of only four deals announced, versus eight and nine during the prior two years, respectively. Indicative of the overall health of the segment, there was only one tuck-in. For the second year in a row, there were no new entrants buying into the segment. Outsiders are either hesitating to invest in direct mail or are unable to convince sellers that the offered price is right. Our perspective is that current owners in the direct mail segment are confident, holding onto their companies, and themselves willing to invest in acquisitions.

Our choice for the notable transaction of the year in the direct mail segment has to be the acquisition of Mailing Services of Pittsburgh (MSP) by Direct Marketing Solutions (DMS). Based in Portland, Oregon, DMS is backed by Main Street Capital, a publicly traded investment firm headquartered in Houston. The combination of the two firms, with private equity backing, is a direct mail powerhouse and indicative of a trend we have noted in which direct mail companies (as well as transactional printing companies) are reaching across the country in their acquisition strategies to mitigate the degradation in postal delivery standards. This transaction was the only one in direct mail over the past year that involved private equity backers. There were no new PE‑backed platforms established in direct mail during the year.

In none of the direct mail transactions did the buyer mention adding a service element as their rationale to move forward with the deal, indicating that the buyers have the services they believe are necessary for now, rather they are adding facilities to increase capacity and expand the company’s footprint within the direct mail business.

Based on the transactional activity, as well as has been discussed with us in private conversations with owners, the direct mail industry appears to be doing quite well, but not on fire from an M&A perspective like packaging, nor are owners beginning an exodus as we believe is and will continue to be the case with many commercial printing company owners.

Transactional activity tells us that an industry segment is undergoing change, however the number of deals does not tell us if that activity is indicative of positive or negative change. To determine a directional indication, we track the number of bankruptcy filings and non-bankruptcy plant closures and correlate this information with the overall transactional activity. Our thesis, born out over several years and confirmed by industry stats derived from other sources, is that an industry segment with a high number of transactions that is also experiencing closures and bankruptcies is, or will be, in a contraction phase. There will be opportunities for consolidation at bargain prices for those companies that defy the downward trend. While this continues to be true in the commercial printing segment, this is less evident than in prior years.

Conversely, segments in which the number of transactions is inversely correlated to closures and bankruptcies are more likely to be expanding. Therefore, consolidation opportunities will come at much higher prices. Virtually all the packaging segments are experiencing steady transactional activity, without the corresponding bankruptcy filings and plant closures, indicating a very healthy environment for sellers as the packaging industry continues to consolidate.

Despite the outbreak of Covid-19 and subsequent difficulties, the number of bankruptcies for the past twelve months across all segments once again decreased compared to prior years. Bankruptcy filings, across all the segments we track, decreased to 22 new filings, down from 29, 38, and 41 over the prior three years, respectively. We believe that this decrease is at least partially, if not mostly, due to the huge cash infusions structured as forgivable PPP loans and other forms of government stimulus. Another factor is likely the high cost of going through a bankruptcy proceeding versus simply winding down a business without the formal filing. As expected, even at the reduced level of bankruptcy filings, the commercial printing segment leads the pack. Of interest, there were no bankruptcies in publishing, presumably the market has been rationalized, at least for the time being. Consistent with our observations above about the wide-format segment, the business appears to be improving and we found only two bankruptcies, down from seven last year.

Our nomination for the most significant bankruptcy filing during the past year is without question the August 6th filing of OSG Group Holdings along with a slew of affiliates and subsidiaries. OSG Billing Services, the predecessor company, was an early star buyer in our Target Report deal logs, beginning in 2014 and appearing no less than eight times. Aquiline Capital acquired the acquisitive OSG in 2017 and continued the roll-up of the transactional printing business, going quiet after the acquisition of Gabriel Group in January 2020. The Chapter 11 bankruptcy was filed as a prepackaged plan with a quick in-and-out of the bankruptcy process. If all goes according to plan, Pemberton Strategic Credit Holdings, the second lien lender, emerges as the new owners in a classic loan-to-own strategy, presumably washing out much or all of Aquiline Capital’s equity value. To many suppliers’ relief, the plan called for unsecured creditors to receive one hundred cents on the dollar of pre-petition debts. The transactional printing segment has been very quiet over the past four years, with no transactions noted in the segment during the past year. That may be about to change as we expect some fallout from even this most orderly of bankruptcies.

Despite the challenges of the past two years, interest in the wide-format segment appears ready to resume as life returns to a post-Covid normal state. A notable example over the past year was the acquisition of Screaming Images, a wide-format printing company in Las Vegas, well-positioned to benefit from the resumption of events in America’s adult playground that doubles as a mecca for trade shows. Geographic diversity was cited by the buyer, Milwaukee-based Olympus Group, as the driving criteria for the purchase. The acquisition brings the company’s footprint to five locations, ranging from Nevada to Florida.

In the wide-format and related products segment, there are proportionately fewer tuck-ins than in general commercial printing. Consistent with the decline in transactional activity over the past two years, there were only two wide-format tuck-ins during the past year, with the seller’s plant shuttered and production consolidated in the buyer’s existing facility. While tuck-ins are usually indicative of excess capacity and with the maturation of the wide-format segment, we frankly expected more transactions as this segment was hit hard. Many wide-format shops pivoted to producing personal protection equipment and warning signage, something that they were especially well-suited for with flatbed cutters and the capability to print floor graphics. Nonetheless, we expect that there are some weaker players in the market and tuck-ins will pick up in this segment.

Only one transaction in the wide-format segment was backed by private equity, the purchase in August of AllOver Media by ShoreView Industries. AllOver Media, based in Minneapolis, specializes in out-of-home advertising including billboards and transportation graphics. The transaction represents a new platform company for ShoreView.

Despite the lull in wide-format transactions, the existing presence of several private equity-backed platforms in the segment portends more activity to come. We continue to believe that the trends in wide-format and related printing, especially the involvement of financial buyers and the smattering of distressed transactions, as noted below, are predictive of increased future M&A activity and consolidation for wide-format printing companies.

Direct mail printing companies, especially those that can manage, manipulate, store, and utilize data to drive improved results for their customers, are an exception and in a class by themselves, apart from the more generalized undifferentiated “job-shop” commercial printing companies that happen to include some mailing capabilities. Therefore, we break out these highly specialized direct mail companies into a separate segment for analysis.

Transactional activity in the direct mail printing segment declined over the past twelve months, with a total of only four deals announced, versus eight and nine during the prior two years, respectively. Indicative of the overall health of the segment, there was only one tuck-in. For the second year in a row, there were no new entrants buying into the segment. Outsiders are either hesitating to invest in direct mail or are unable to convince sellers that the offered price is right. Our perspective is that current owners in the direct mail segment are confident, holding onto their companies, and themselves willing to invest in acquisitions.

Our choice for the notable transaction of the year in the direct mail segment has to be the acquisition of Mailing Services of Pittsburgh (MSP) by Direct Marketing Solutions (DMS). Based in Portland, Oregon, DMS is backed by Main Street Capital, a publicly traded investment firm headquartered in Houston. The combination of the two firms, with private equity backing, is a direct mail powerhouse and indicative of a trend we have noted in which direct mail companies (as well as transactional printing companies) are reaching across the country in their acquisition strategies to mitigate the degradation in postal delivery standards. This transaction was the only one in direct mail over the past year that involved private equity backers. There were no new PE‑backed platforms established in direct mail during the year.

In none of the direct mail transactions did the buyer mention adding a service element as their rationale to move forward with the deal, indicating that the buyers have the services they believe are necessary for now, rather they are adding facilities to increase capacity and expand the company’s footprint within the direct mail business.

Based on the transactional activity, as well as has been discussed with us in private conversations with owners, the direct mail industry appears to be doing quite well, but not on fire from an M&A perspective like packaging, nor are owners beginning an exodus as we believe is and will continue to be the case with many commercial printing company owners.

Challenged Segments

Transactional activity tells us that an industry segment is undergoing change, however the number of deals does not tell us if that activity is indicative of positive or negative change. To determine a directional indication, we track the number of bankruptcy filings and non-bankruptcy plant closures and correlate this information with the overall transactional activity. Our thesis, born out over several years and confirmed by industry stats derived from other sources, is that an industry segment with a high number of transactions that is also experiencing closures and bankruptcies is, or will be, in a contraction phase. There will be opportunities for consolidation at bargain prices for those companies that defy the downward trend. While this continues to be true in the commercial printing segment, this is less evident than in prior years.

Conversely, segments in which the number of transactions is inversely correlated to closures and bankruptcies are more likely to be expanding. Therefore, consolidation opportunities will come at much higher prices. Virtually all the packaging segments are experiencing steady transactional activity, without the corresponding bankruptcy filings and plant closures, indicating a very healthy environment for sellers as the packaging industry continues to consolidate.

Despite the outbreak of Covid-19 and subsequent difficulties, the number of bankruptcies for the past twelve months across all segments once again decreased compared to prior years. Bankruptcy filings, across all the segments we track, decreased to 22 new filings, down from 29, 38, and 41 over the prior three years, respectively. We believe that this decrease is at least partially, if not mostly, due to the huge cash infusions structured as forgivable PPP loans and other forms of government stimulus. Another factor is likely the high cost of going through a bankruptcy proceeding versus simply winding down a business without the formal filing. As expected, even at the reduced level of bankruptcy filings, the commercial printing segment leads the pack. Of interest, there were no bankruptcies in publishing, presumably the market has been rationalized, at least for the time being. Consistent with our observations above about the wide-format segment, the business appears to be improving and we found only two bankruptcies, down from seven last year.

Our nomination for the most significant bankruptcy filing during the past year is without question the August 6th filing of OSG Group Holdings along with a slew of affiliates and subsidiaries. OSG Billing Services, the predecessor company, was an early star buyer in our Target Report deal logs, beginning in 2014 and appearing no less than eight times. Aquiline Capital acquired the acquisitive OSG in 2017 and continued the roll-up of the transactional printing business, going quiet after the acquisition of Gabriel Group in January 2020. The Chapter 11 bankruptcy was filed as a prepackaged plan with a quick in-and-out of the bankruptcy process. If all goes according to plan, Pemberton Strategic Credit Holdings, the second lien lender, emerges as the new owners in a classic loan-to-own strategy, presumably washing out much or all of Aquiline Capital’s equity value. To many suppliers’ relief, the plan called for unsecured creditors to receive one hundred cents on the dollar of pre-petition debts. The transactional printing segment has been very quiet over the past four years, with no transactions noted in the segment during the past year. That may be about to change as we expect some fallout from even this most orderly of bankruptcies.

And finally, we also track activity in non-bankruptcy plant closures; some companies simply close up and just disappear while others find a buyer for the book-of-business and conduct an orderly wind-down process. A closure does not always mean that the company has ceased operating, it may simply be that one of the larger printing firms is rationalizing their production capacity. Either way, closures are indicative of change, usually resulting from downward pressure in a market segment.

Consistent with the bankruptcy filing data, the number of non-bankruptcy closures in the past twelve months declined to 23, down from 33, 45, and 49 over the past three years, respectively.

As expected, general commercial printing companies represent the majority of printing facilities closing up shop. newspaper printing plants also closed in greater numbers than most other segments. Similar to our conclusion from the data on bankruptcy filings, we did not find any printing companies that closed up that were primarily in the publication or catalog printing business. However, we still hear of major titles ceasing to publish the printed edition, moving the content to a digital online experience, suggesting will be difficulties ahead in this segment as more titles go online only.

As expected, general commercial printing companies represent the majority of printing facilities closing up shop. newspaper printing plants also closed in greater numbers than most other segments. Similar to our conclusion from the data on bankruptcy filings, we did not find any printing companies that closed up that were primarily in the publication or catalog printing business. However, we still hear of major titles ceasing to publish the printed edition, moving the content to a digital online experience, suggesting will be difficulties ahead in this segment as more titles go online only.

| 2022 August - Mergers and Acquisitions in the Printing, Packaging, Paper & Related Industries | |||||||||||||

Deal Party #1 (Surviving Entity) |

Pre-Deal Revenue (US$Mil) |

Party #1 Address |

Deal Party #2 |

Pre-Deal Revenue (US$Mil) |

Party #2 Address |

Date Deal Public |

Deal Value (US$Mil) |

Deal Structure (Intermediary) |

Notes |

Link | |||

| Ironmark (Port co. Post Capital Partners) |

No Data | Annapolis Junction, MD | Millennium Marketing Solutions | No Data | Annapolis Junction, MD | 8/31/22 | No Data | Acquisition (Graphic Arts Advisors) |

Marketing & branding services | Link | |||

| Open Jar Studios | No Data | New York, NY | Bway Printing | No Data | New York, NY | 8/30/22 | No Data | Acquisition | Printing & copying | Link | |||

| Fortis Solutions Group (Port co. Harvest Partners) |

No Data | Virginia Beach, VA | Identi-Graphics | No Data | Montgomery, IL | 8/30/22 | No Data | Acquisition | Labels & flexible packaging | Link | |||

| Aurelius Group | No Data | Grünwald, Germany | Offset Solutions Business (Div. Agfa-Gevaert) |

$747.3 | Mortsel, Belgium | 8/30/22 | $91.9 | Acquisition | Prepress supplies | Link | |||

| Incline Equity | No Data | Pittsburgh, PA | NovaVision | No Data | Bowling Green, OH | 8/30/22 | No Data | Acquisition | Security tapes & labels | Link | |||

| ShoreView Industries | No Data | Minneapolis, MN | AllOver Media | No Data | Minneapolis, MN | 8/24/22 | No Data | Acquisition | Out-of-Home advertising | Link | |||

| Solar Art | No Data | Laguna Hills, CA | Brower Tinting & Graphics | No Data | Renton, WA | 8/22/22 | No Data | Acquisition | Window graphics | Link | |||

| Heath & Tasha Sullivan | No Data | Cleveland, TN | Carroll Printing | No Data | Cleveland, TN | 8/20/22 | No Data | Acquisition | Printing & copying | Link | |||

| Ennis | $410.8 | Midlothian, TX | Gulf Business Forms | No Data | San Marcos, TX | 8/17/22 | No Data | Acquisition | Business forms | Link | |||

| Millcraft Paper | No Data | Cleveland, OH | KW Graphics | No Data | Springfield, IL | 8/16/22 | No Data | Acquisition | Binding supplies & equipment | Link | |||

| Saati | No Data | Appiano Gentile, Italy |

Ikonics (Sub. TeraWulf) |

No Data | Duluth, M | 8/15/22 | No Data | Acquisition | Imaging technologies | Link | |||

| Specialty Printing & Marketing | No Data | Shepherdstown, WV | Grubb Printing & Stamp Co | No Data | Portsmouth, VA | 8/15/22 | No Data | Acquisition (Corp Dev Assoc) |

Commercial printing | Link | |||

| Dallas Plastics (Port co. Sole Source Capital) |

No Data | Mesquite, TX | MPP Packaging | No Data | Montreal, QC | 8/15/22 | No Data | Acquisition | Packaging films | Link | |||

| BR Printers | No Data | San Jose, CA | Egan Printing | No Data | Denver, CO | 8/12/22 | No Data | Acquisition | Commercial printing | Link | |||

| Esko (Sub. Danaher) |

No Data | Ghent, Belgium | Tilia Labs | No Data | Ottawa, ON | 8/10/22 | No Data | Acquisition | Graphic production software | Link | |||

| Charter Next Generation | No Data | Milton, WI | Polymer Film & Bag (Div. Polymer Packaging) |

No Data | Massillon, OH | 8/8/22 | No Data | Acquisition | Bags & packaging films | Link | |||

| Cox Enterprises | No Data | Atlanta, GA | Axios | No Data | Arlington, VA | 8/8/22 | $525.0 | Acquisition | Online news | Link | |||

| Eukalin | No Data | Eschweiler, Germany |

Adhesives Specialists | No Data | Allentown, PA | 8/8/22 | No Data | Acquisition | Specialty adhesives | Link | |||

| CenterGate Capital | No Data | Austin, TX | Prisma Graphic | No Data | Phoenix, AZ | 8/4/22 | No Data | Acquisition | Commercial printing | Link | |||

| Labelink | No Data | Anjou, QC | The Label Factory | No Data | Georgetown, ON | 8/3/22 | No Data | Acquisition | Label printing | Link | |||

| Labelink | No Data | Anjou, QC | Taylor Label | No Data | Brampton, ON | 8/3/22 | No Data | Acquisition | Label printing | Link | |||

| The Southeast Iowa Union (Div. Folience) |

No Data | Cedar Rapids, IA | Belle Plaine Star Press Union (4 titles) (Prop. Gannett) |

No Data | Belle Plaine, IA | 8/3/22 | No Data | Acquisition | Community newspapers | Link | |||

| DazPak Flexible Packaging (Port co. H.I.G. Capital) |

No Data | Commerce, CA | Inno-lok (Div. Polymer Packaging) |

No Data | Massillon, OH | 8/2/22 | No Data | Acquisition | Flexible packaging | Link | |||

| DazPak Flexible Packaging (Port co. H.I.G. Capital) |

No Data | Commerce, CA | Atlapac | No Data | Columbus, OH | 8/2/22 | No Data | Acquisition | Flexible packaging | Link | |||

| 2022 August - Bankruptcy Filings in the Printing, Packaging, Paper & Related Industries | ||||||||||||

Filing Party |

Date Case Filed |

Pre-Petition Revenue (US$Mil) |

Case # |

Filing Party Address |

Circuit |

Region & City |

Judge |

Attorney for Debtor |

Notes |

|||

| Chapter 11 Filings: | ||||||||||||

| OSG Group Holdings (Port co. Aquiline Capital) |

8/6/22 | No Data | 22-10718 | Carlstadt, NJ | 3rd | Delaware Wilmington |

John T. Dorsey | Erin R. Fay | Transactional printing | |||

| Chapter 7 Filings: | ||||||||||||

| No Chapter 7 Filings Found this Month | --- | --- | --- | --- | --- | --- | --- | --- | --- | |||

| 2022 August - Non-Bankruptcy Closures in the Printing, Packaging, Paper & Related Industries | |||||||||||

Closed Company / Facility |

Date of Closure |

Pre-Closure Revenue (US$Mil) |

Closing Address |

Related Party | Related Party Address |

Date Closure Public | Notes |

Press Releases |

|||

| Cover Material Sales | 9/8/22 | No Data | Hyannis, MA | None | N/A | Aug-22 | Book cover material converting | Link | |||